Published On Sep 4, 2019

Price Stock Options with Monte Carlo Simulation in Excel*

Please SUBSCRIBE:

https://www.youtube.com/subscription_...

Download the spreadsheet model at the link below:

https://alphabench.com/data/excel-mcs...

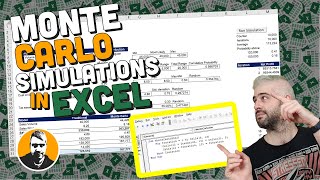

Walk-through of valuing European style options with Monte Carlo simulation. We build a spreadsheet model that estimates stock ending prices based on a deviation of the Black Scholes Merton pricing model. Ending prices are then used to value either a call or put option with a specific strike price.

This tutorial assumes a basic knowledge of stock option contracts.

European options can only be exercised at expiration, while American style options can be exercised at any time. This makes American options somewhat more valuable than European options to account for the additional exercise risk. The additional premium is between about 5% and 10% for American options.

*The content is for informational purposes only. Investment in option securities can involve the risk of losing any monies invested. This video and other content should not be construed as investment, financial, or other advice.

#options #montecarlo #stock